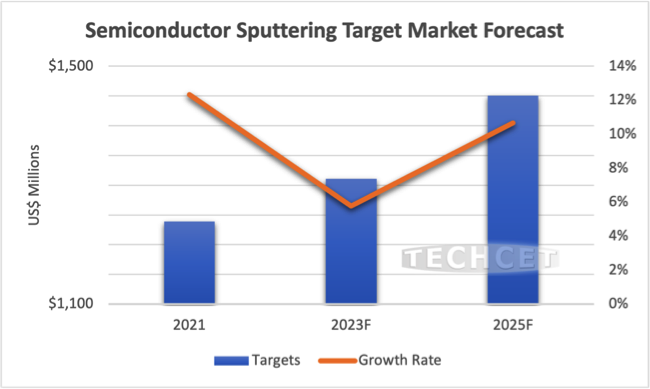

TECHCET—the electronic materials advisory firm providing business and technology information— announced that the Semiconductor Sputtering Target market is expected to reach US$1.33 billion in 2022, up 7% from US$1.24 billion in 2021. Target suppliers are planning for 2023 deliveries to remain on track to meet high forecasted customer demand. TECHCET also forecasts a slight decline of -1.1% YoY for 2023, due to inventory corrections, as shown below.

As highlighted in the newly released 2022 Sputtering Targets Critical Material Report™, target suppliers indicate that the supply/demand balance for Copper/Copper Alloy targets remains very tight. While new investments have been announced to boost Copper target manufacturing capacity, these will take time to ramp as manufacturing equipment lead-times can be one-year or more. For the year of 2022, the Copper/Copper Alloy target segment is forecasted to grow 11% in revenues. Some suppliers now report the focus is on delivering forecasted target volumes to meet 2023 customer demand.

The metal supply chain appears to be stable, although metal pricing did see a surge in 2021 and into early 2022. Unfortunately, near-term recession fears have resulted in recent price declines for commodity metals. In the future, demand for many metals used for chip production is predicted to be especially strong given broader application drivers. This has created uncertainty in predicting longer-term supply and pricing for metals.

“Globally, ‘green’ economy and zero emissions initiatives have boosted the need for increasing mining production to meet targeted projections for needed electrification infrastructure,” states Dan Tracy, senior analyst at TECHCHET. For example, copper metal demand could double between now and 2035-2040, so significant investments are needed to increase Copper mining production. While copper usage in semiconductor target fabrication is negligible compared to other applications, any future supply issues will still mean higher pricing for targets.

In addition to copper, new mining activity for Cobalt, Tungsten, Silver and other materials will need to expand so industries can satisfy green economy/zero emissions objectives. New mining developments can take 15 years or more, so any supply/demand imbalance could also result in higher commodity metal pricing. As these initiatives move forward, recycle, reclaim, and reuse will be critical components of most metal supply chains – including sputtering targets.

While current metal supply is generally viewed as being stable, higher energy costs are also impacting the mining, smelting, and refining of metals in the near-term, and customers will encounter surcharges due to these factors.