Despite some cyclicality and seasonality, the stand-alone memory market has experienced extraordinary growth over the past decade. This has been driven by important megatrends, such as mobility, cloud computing, AI, and IoT.

“NAND and DRAM account together for around 97% of the overall stand-alone memory market,” announced Simone Bertolazzi, Market & Technology Analyst, Memory at Yole Développement (Yole). “Their revenues hit a record high of around US$160 billion in 2018, registering an impressive CAGR of 32% between 2016 and 2018.”

Yole Group of Companies including Yole, System Plus Consulting and Knowmade is daily working with the leading memory players to collect valuable market and technology data. Memory analysts collaborate with them to understand their vision of the industry and evaluate the market growth and technological evolution on an ongoing basis. Yole Group’s knowledge is now proposed through a wide collection of reports and monitor services.

Memory market & technology reports provide an overview of the industry, with a detailed analysis of the technology challenges, devices’ trends and a deep understanding of the supply chain with an accurate players mapping. Status of the Memory Industry report is the latest memory study published by Yole. This study proposes a comprehensive overview of the memory industry with a detailed description of the technologies and devices and competitive landscape. Under this new report, Yole’s analysts reveal today their vision of each market segment and related applications to highlight the impact of the megatrends and market drivers. This report also includes a large section focused on forecasts and roadmaps.

In addition, memory analysts reveal the status of the memory business each quarter with the DRAM & NAND Quarterly Market Monitor services. These services provide an accurate outlook of the market, its current status, and near- and long-term outlooks.

Counting for more than one third of the whole semiconductor market today, the memory business is key for numerous companies, from substrate to devices, including modules and systems makers. What could happen in a near future? In a long-term? Yole Group of Companies is following issues and innovations to give you a better understanding of the industry evolution.

At the end of 2018, both NAND and DRAM markets started experiencing oversupply caused by unseasonably weak demand, including lower than- expected smartphone sales and a slowdown in datacenter demand:

“DRAM prices are projected to decline by around 40% this year and likely will not increase again until 2020,” asserted Mike Howard, VP of DRAM and Memory Research at Yole.

“For NAND, hopes of a second-half 2019 market rebound are shrinking as the anticipated demand recovery continues to be elusive and supplier inventory levels remain elevated,” adds Walt Coon, VP of NAND and Memory Research at Yole. See the Quarterly DRAM & NAND snapshot: From bad to worse in Q1 2019 published on i-micronews.com.

As part of the NAND business, 3D NAND technology is showing impressive developments…

“To answer to the impressive demand for higher storage capacity and reliability while lowering cost per bit, 3D NAND manufacturers implements innovative techniques,” explains Belinda Dube, Cost Analyst at System Plus Consulting. “They change the storage type, the memory cell design and stack more layers with each generation to increase bit density hence reducing the die sizes. The technological changes in the cell architecture and modification of the fundamental memory features add complexity to the manufacturing process. However these techniques do lower the cost per gigabyte.”

System Plus Consulting is following the evolution of memory technologies with a collection of reverse engineering and costing reports. With the Leading-edge 3D NAND Memory Comparison 2018 the team presents a technological and economical comparison of the latest generation of 3D NAND solutions available on the market from four different manufacturers. These are the 64-layer designs from Toshiba/SanDisk, Samsung and Intel/Micron and the 72-layer 3D NAND by SK Hynix.

In the long-term, NAND and DRAM revenues are forecast to grow with 4% and 1% CAGR respectively, between 2018 and 2024. This is thanks to ever-growing bit demand fueled by novel AI/IoT applications and systems, such as smart cities, connected homes and intelligent factories, smartphones and Echo-like personal assistants, virtual and augmented reality and autonomous vehicles. All these rely on a massive amount of data and on the networks that connect them all. Thus, the coming rollout of 5G wireless technology will be critical for their future market expansion.

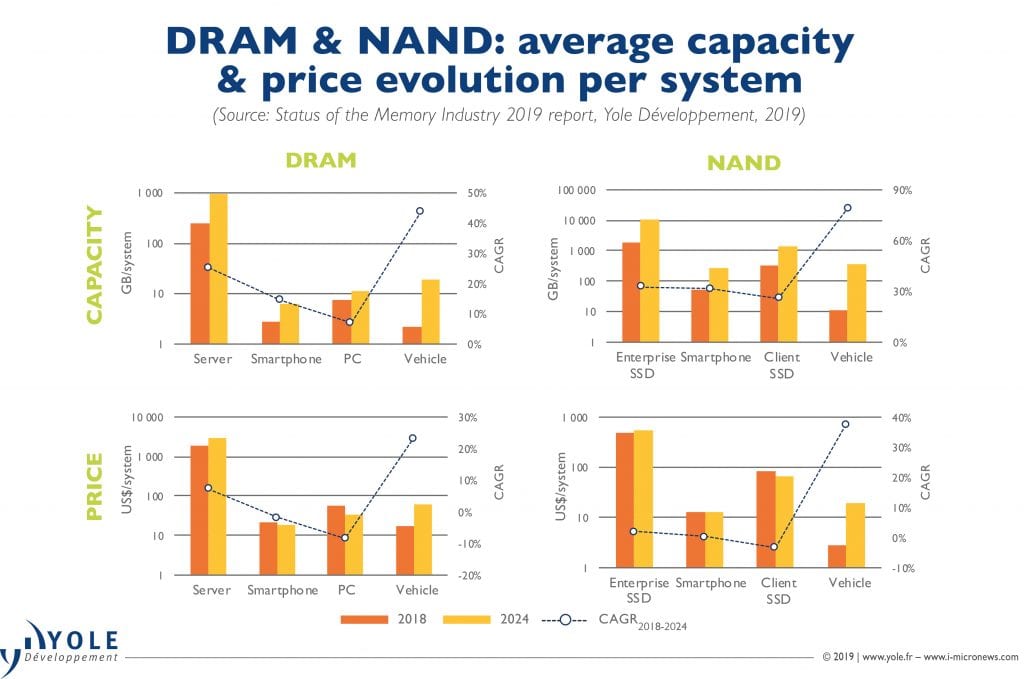

Under the Status of the Memory Industry report, Yole’s memory team carried out a systematic study of the evolution of memory requirements in various key systems, including servers, smartphones, PCs, enterprise/client SSDs , and vehicles. Servers and enterprise SSDs for datacenters are the most important bit-consuming systems for DRAM and NAND memory, respectively. On the other hand, automotive is the fastest growing segment. The amount of bits in cars is expected to grow by orders of magnitude due to increasing penetration of ADAS for autonomous vehicles.

Notably, eNVM started making inroads into the SCM market with the introduction in 2017 of Intel’s Optane PCM products. As the new generations of Xeon server CPUs are conceived to be compatible with the new Optane persistent memory modules (NVDIMM), Intel might be able to gain significant business at the expense of Samsung and SK Hynix, who are now getting ready with their own PCM products.