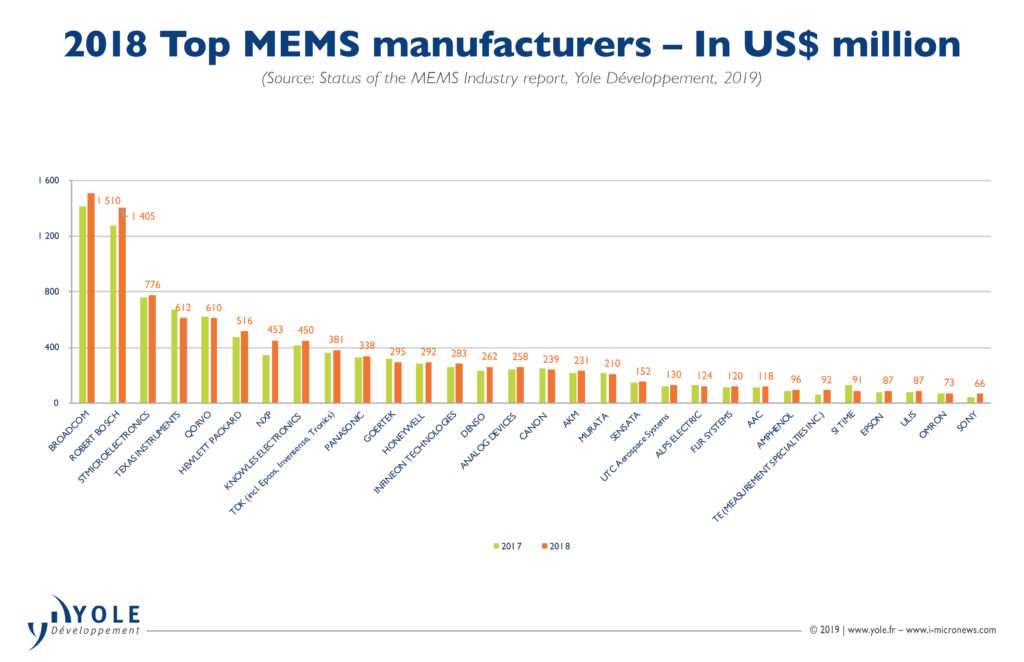

For another year, Broadcom and Robert Bosch (Bosch) remain the global MEMS leaders. Almost every player exhibited a stable yearly growth (From 2017 to 2018) though a bit weaker than the previous period (From 2016 to 2017).

Yole Développement (Yole) believes that this smaller than expected growth of the MEMS players during 2018 reflects a modest re-adjustment of growth of the semiconductor industry. Do not get us wrong: 2018 was the best year so far for the semiconductor industry in general. However, its growth was about 15% between 2017 and 2018, comparatively smaller than the almost 21% growth in the 2016-2017 period. This is probably associated with the fact that during the last quarter of 2018, smartphone and automotive sales were impaired, causing an inventory build-up, both end products and MEMS.

The market research and strategy consulting company, Yole expect this build-up to burn-out early 2019 (Q1-Q2), followed by a moderate MEMS growth for the rest of the year.

The Photonic, Sensing & Display team from Yole is following the MEMS industry for more than 20 years. Each year, analysts propose a comprehensive technology & market analysis focused on the MEMS market, its technical innovations, its competitive landscape and more. Yole announces today its annual Top 30 MEMS manufacturers and reveals the status of the MEMS industry.

For 2018, Broadcom still holds the top position in MEMS. In the previous year’s ranking, Yole’s team overestimated its growth due to an order that would supposedly ship at the end of 2017 but was delayed to the following year. However, even if mobile phone shipments slowed down during 2018, growth continued for RF driven by an increasing number of filters, in conjunction with the front-end module’s increasing value. The introduction of 5G will further drive this prosperity. While we also expected growth for another big RF player, Qorvo, this didn’t happen. Qorvo experienced a small revenue decline despite transitioning from 6” to 8” platform (probably causing a delay in production).

“Bosch saw a more than US$100 million increase in revenue due to its strong presence in consumer (#1 player) and automotive markets,” explained Dimitrios Damianos, PhD., Technology & Market Analyst at Yole. “Every new vehicle contains an average of 5 Bosch MEMS, while half of the world’s smartphones have at least 1 Bosch MEMS.”

With the exception of NXP and Sony, which grew by 30% and 40% correspondingly, most of the companies profited from a stable growth ranging from a modest 2% up to a great 10-15%:

• The revenues of Inkjet Head players like Canon and HP rose while Epson shrank. HP recovered in the consumer printer market which has been declining during the previous years.

• Concerning the MEMS microphone giants, Knowles thrived (due to its good consumer business, which is not limited to smartphones but headsets, etc.) while Goertek declined, most probably due to the weakened global mobile phone sales. AAC also grew.

• On the microbolometer front, FLIR and ULIS continue to grow year after year due to a multitude of applications (with the most important being personal vision systems, firefighting, drones as well as legacy thermography and military, surveillance).

Formfactor is out of the ranking while Sony entered, though in the bottom position. First Sensor, which is in advanced takeover talks with TE Connectivity, missed entering the top 30 by a hair’s breadth.

“In 2017, the TOP 30 MEMS players’ revenues were US$9.88 billion,” asserts Eric Mounier, PhD., Fellow Analyst at Yole. “In 2018, they totaled more than US$10.3 billion, almost a 5% YoY growth. These players comprise 90% of the total MEMS market, which in 2018 was more than US$11.6 billion.”

The YoY% spikes during the 2016/2017 period for Amphenol, Denso and Sensata are due to an updated estimation of their MEMS revenues at first level packaging only.

The YoY% spike for TE arises from an underestimation of their revenue during 2016/2017 due to limited MEMS portfolio knowledge. This was readjusted for the period 2017/2018.

For SiTime, the YoY% spike during 2016/2017 was because their revenue was overestimated due to belief of more MEMS oscillators shipments but readjusted during 2017/2018. TI is still losing revenue.

TI’s DLP are still constrained to consumer projection applications – waiting possible uses in LIDAR, heads-up displays (HUD) and smart headlights.

All MEMS market segments, including Inkjet heads, pressure, microphones, inertial, optical MEMS, microfluidics, RF, and more …, are analyzed in-depth in Yole’s annual report, Status of the MEMS Industry. A full description of this technology & market analysis is available in the MEMS & Sensor reports section, on i-micronews.com.

In addition, Yole’s team will attend Sensors Expo. & Conference from June 25 to 27. Make sure to meet Yole and System Plus Consulting team on booth 343 and assist the presentation of Dimitrios Damianos, MEMS & Sensors and Imaging Market and Technology Analyst at Yole: “Get the Relevant Quantitative Data on Autonomous Vehicle Sensors & Sensor Fusion” on June 25 at 10:15 AM (Market Analyst View session). More info. on i-micronews.com.