WALT COON and MIKE HOWARD, Yole Développement, France

It is easy to imagine how a global pandemic that results in widespread lockdown might negatively impact demand. Perhaps a more illuminating question is if there are any demand segments that have been positively impacted by COVID-19. The short answer is yes. One of the big winners during this crisis has been datacenter, and we thought we would share a few anecdotes that illustrate this.

The first example is Netflix. Over the last eight years Netflix has averaged about four and a half million new customers per quarter. In Q1-20 much of the world went on lockdown and we saw a huge surge in media streaming. The result was that in Q1-20 Netflix had nearly 16 million new users – more than three times their average and 60% more than their prior record – and Q1 only had a few weeks of lockdown for much of North America and Europe. Clearly this has been a boon for streaming media and the datacenters that host streaming media.

Another area where we have seen surging demand is gaming. Steam, the online gaming platform, averaged about 16 million users per day over the six months prior to lockdown. During lockdown it has averaged 23 million users per day, a nearly 50% jump in demand.

Other categories that have been driving datacenter demand include online shopping and video conferencing services such as Zoom and WebEx, which are taking the place of face-to-face interaction as to the world adjusts to “work from home”.

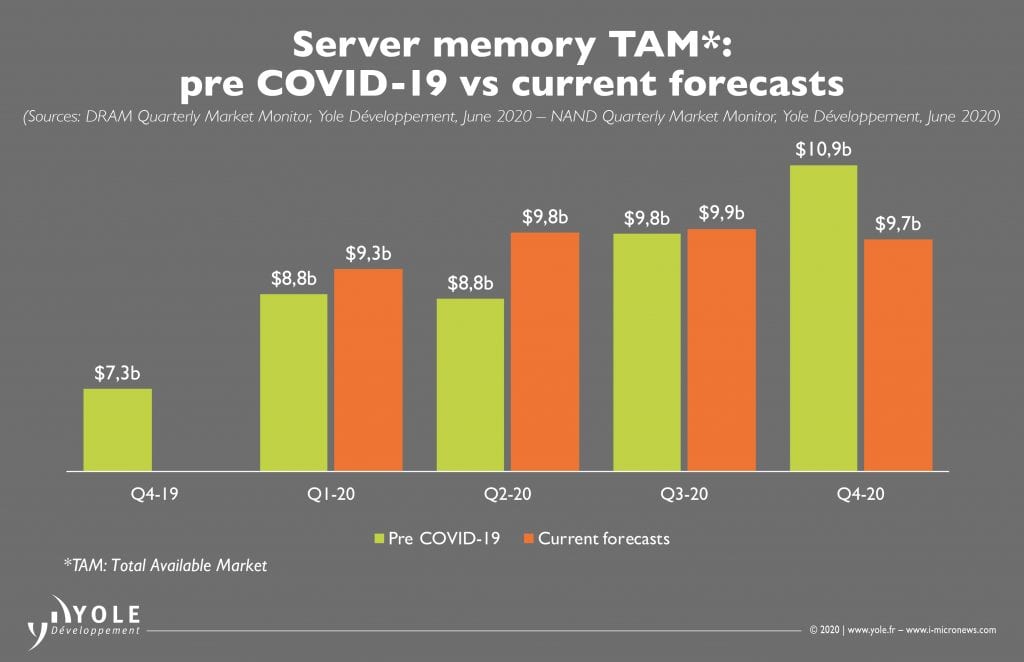

Before COVID we expected the Datacenter to generate about $38 billion in memory revenue in 2020, with revenue weighted towards the second half of the year. Today we anticipate slightly higher revenue but split evenly between the first and second half of the year. Essentially, the first-half surge in demand has changed the half-on-half dynamics for 2020. Cloud Service Providers have been big buyers thus far this year as they have seen significant upticks in demand and have grown inventory to hedge against any potential supply chain disruptions that might arise due to COVID. Further, traditional enterprise has been scrambling to assess “work from home” and budgets have not been cut at this stage (FIGURE 1).

There is, however, ample uncertainty about the second half of 2020. We expect traditional enterprise to reduce spending as the full economic impact of COVID is better understood. Additionally, although CSPs have been big drivers of first half demand, there is concern that shrinking ad revenues, overly robust memory inventories, and general economic malaise will prompt a spending cut in the second half.

PCs

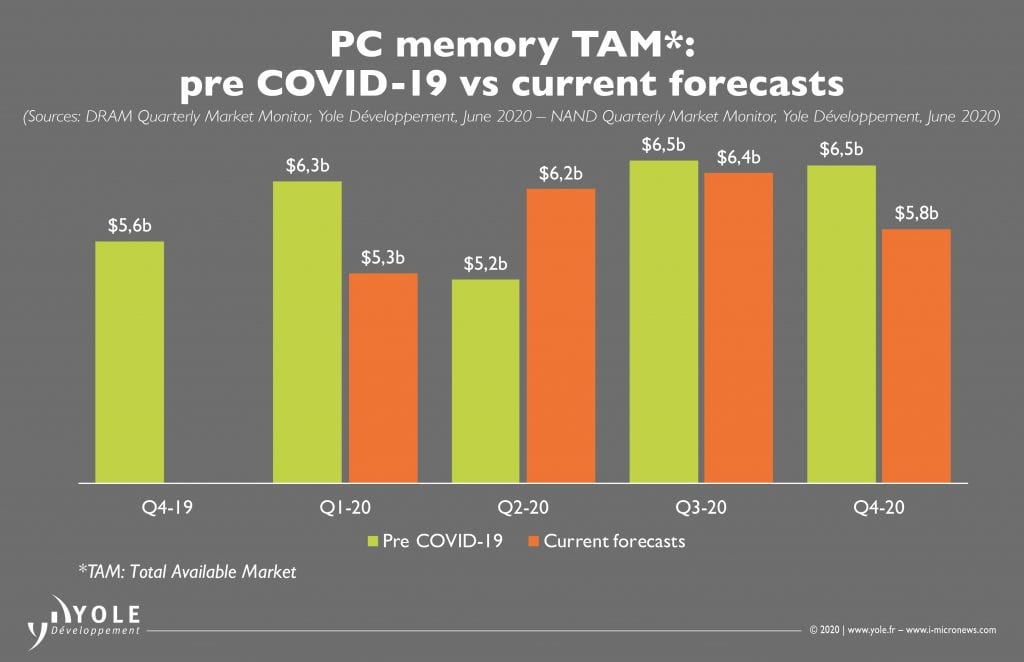

Another category which we believe will fare relatively well during the COVID pandemic is PCs. Our pre-COVID forecast was for ~$24.5 billion to be spent on memory for PCs and our current outlook is only down about $1B from this level. While Q1 PC unit sales were much lower than anticipated, much of that was due to supply chain constraints rather than a lack of demand. Those constraints have now been resolved and we expect Q2 sales of PCs to be up quite dramatically.

Clearly “work from home” is causing the surge in PC demand as people realize that getting real work done – especially for extended durations – requires the right equipment. This surge in PC demand is likely a one-time uplift in demand and not a systemic change to the PC market. (FIGURE 2).

For the year, we have reduced our PC unit forecast about 1%. Even though we are seeing strong demand today as people attempt to work from home, we expect PC sales in the second half of 2020 to suffer as economic headwinds take hold, people working from home have made the needed upgrades, and enterprise looks to tighten budgets.

Smartphones

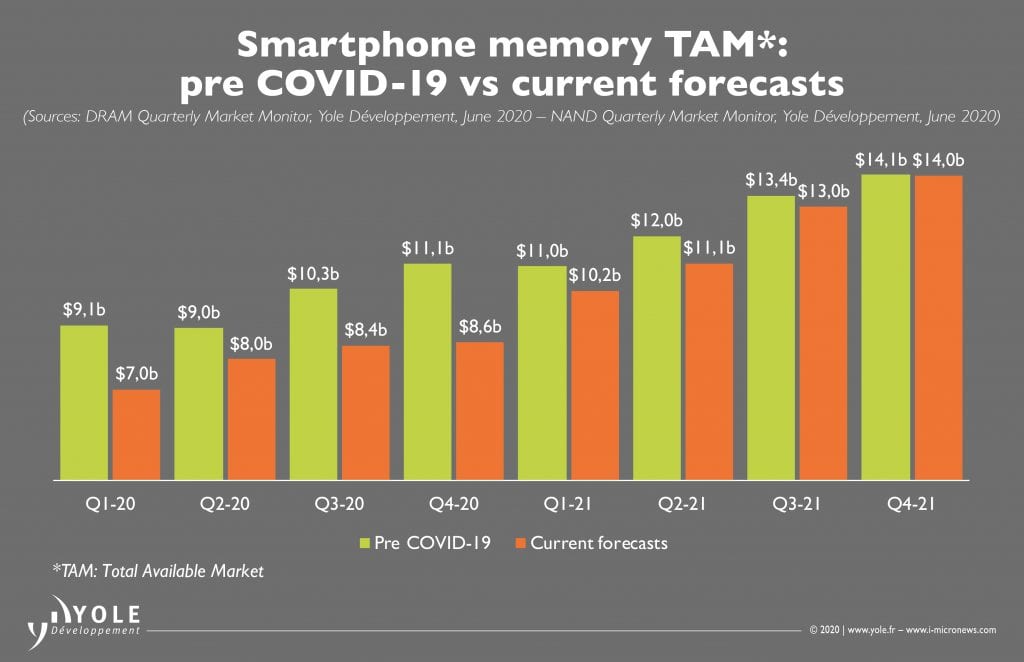

Smartphones is the category that has been the most adversely impacted by COVID. At the beginning of the year we expected 2020 to be a strong year for smartphones. With enthusiasm around 5G driving an upgrade cycle, we expected new smartphone shipments to be around 1.4 billion units and memory revenue to reach nearly $40 billion growing to $50 billion next year. Today we expect smartphone shipments to come in around 1.1 billion and memory revenue to be about 20% lower at $32 billion in 2020 before recovering in 2021 (FIGURE 3).

People’s inability to get out and shop for a new phone during lockdown, coupled with economic uncertainty and hardship, has resulted in people holding onto old phones for longer and postponing upgrades. However, we believe that long-term the segment will bounce back. Phones do not last forever and there is not currently a substitute device for smartphones (as the smartphone was the replacement device for the PC ten years ago). Therefore, eventually old phones will need to be replaced. This will result in “catch up” demand which we expect to start seeing in 2021. We anticipate the smartphone market will perform very well next year.

Memory supplier reactions

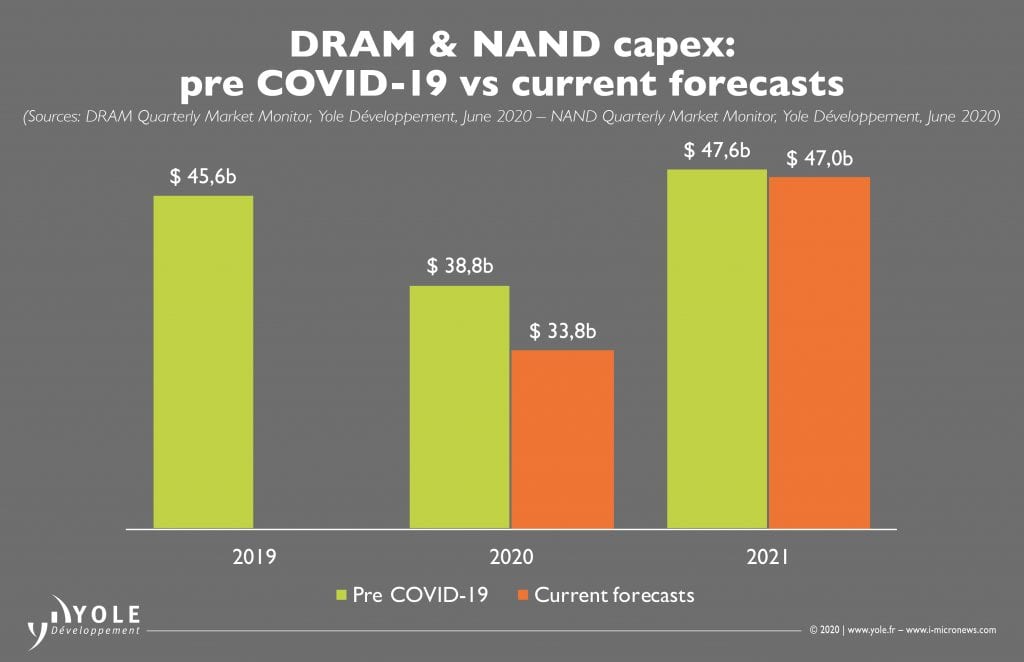

Capital expenditures Prior to the COVID-19 outbreak expectations were for combined DRAM and NAND capital expenditures (capex) of $38.8 billion in 2020, down 15% year-over-year, including both WFE and infrastructure spend. This decrease was a result of the memory market downturn that plagued 2019—and much of 2018 for NAND—as well as the timing of infrastructure build outs and technology transitions.

The current forecast assumes a much steeper 2020 capex drop-off, with combined DRAM and NAND capex of $33.8 billion, down 26% from 2019 and 13% lower than the prior outlook. It is expected that the memory suppliers will be more cautious with investments this year due to the uncertainty around second half demand and longer-term economic ramifications. The memory suppliers are likely to err on the side of caution and push spend into 2021 or potentially further depending on market conditions (FIGURE 4).

The ramifications of reduced capex are significant. Lower capex equates to slower technology transitions, fewer new wafer additions, diminished bit growth, and reduced cost per bit declines. Smaller cost declines may lead to lower profit margins and lower revenue TAM, depending on the impacts to memory average selling prices (ASPs). Given the uncertainty in the market, reducing capex in the near-term appears to be a prudent decision. The suppliers can hope that lower capex (and therefore lower bit shipments) will result in higher ASPs, offsetting smaller cost per bit declines.

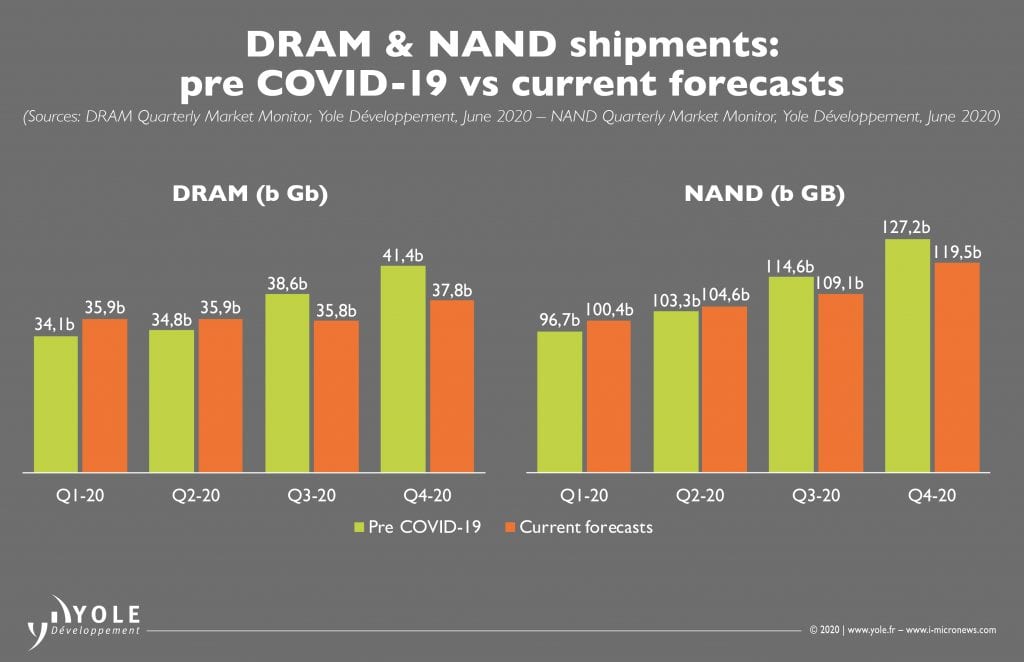

Memory supply The impacts from the pandemic were felt by the memory suppliers almost immediately and have been reflected in first half bit shipments for both DRAM and NAND. The widespread work- and learn-from-home transition has provided a near-term boost to the memory suppliers, leading to first half memory bit shipments higher than previously anticipated. Shipment growth has been led by strong server and PC demand and customer buy-aheads due to supply chain concerns, which have helped offset initial COVID-related weakness in the smartphone and consumer markets.

Looking ahead to the rest of the year, although datacenter demand is expected to remain resilient, we anticipate continued weakness in the smartphone and consumer markets and softening PC demand after the initial surge from the first half wanes. Demand for traditional enterprise servers is also at risk, as economic uncertainty may lead to more conservative IT spend. As a result, second half 2020 bit shipment expectations have been lowered for both DRAM and NAND (FIGURE 5).

The impact to NAND bit shipments is not expected to be as significant as DRAM for a several reasons. Prior to the outbreak, 2020 NAND bit growth was already expected to be constrained, with the market just emerging from a major downturn and supply impacts from previous capex cuts taking hold. Additionally, NAND has the continued benefit of the HDD-to-SSD replacement cycle in PC’s, with the current PC demand surge coming from corporate buyers who overwhelmingly use SSD-based storage along with Chromebooks on the education side using NAND-based storage. Finally, the introduction of new gaming consoles later this year, which are shifting from HDD to high density SSD-based storage solutions, will provide a significant boost to bit demand in the second half.

For the full year, DRAM bit growth (2020 vs. 2019) has been lowered from 17% in the prior forecast to 15%, while NAND bit growth has been lowered from 30% to 29%.

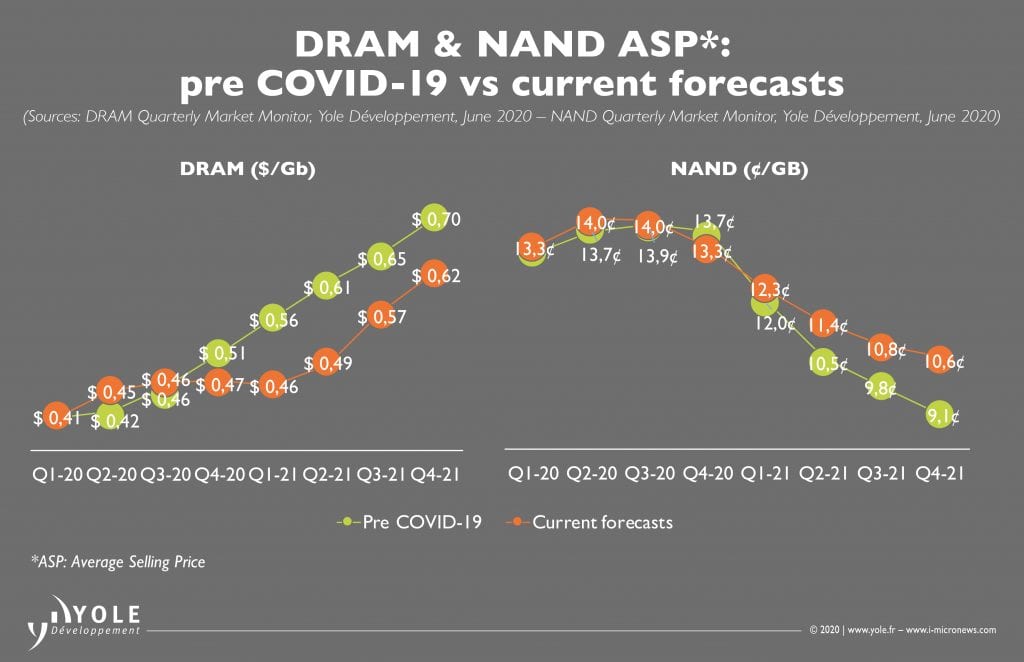

Memory pricing Strength in datacenter and PC demand has led to higher-than-anticipated pricing for both DRAM and NAND in the first half of 2020. However, weaker demand in the second half is likely to reduce pricing relative to prior expectations. The reality is that second half pricing will be largely dictated by the response of the suppliers to this pandemic. Will they adjust wafer output and technology transitions in the face of demand uncertainty, or continue along the path of their prior plans? There are several actions the supplier can take to bolster pricing in the face of demand uncertainty, including reducing capex, lowering fab utilization, and holding strategic inventory.

Strong datacenter demand has driven server DRAM pricing up ~40% since the end of 2019. Server DRAM prices, however, are not likely to rise much more in 2020 as large CSPs have ample inventory and the availability of server DRAM should be greater in the second half of 2020 as suppliers have shifted wafers from mobile DRAM to compute. The surge in H1 2020 pricing will result in overall pricing for the year being slightly better than previously expected but 2021 prices are not expected to climb as high due to the drag on demand from the anticipated economic fallout (FIGURE 6).

The NAND downturn that spanned most of past few years resulted in steep losses for the industry in 2019. Although industry margins moved positive in Q1 2020, there is little room for large price declines in the coming quarters. Additionally, capex reductions will impact the ability of the NAND suppliers to lower costs both this year and beyond. As a result, the full year outlook for blended NAND pricing in 2020 is mostly unchanged, with pricing expected to be up 6% year-over-year. Based on the current forecast, long term NAND industry margins are not sustainable, and the industry likely needs to see consolidation or some other structural shift to generate sufficient returns.

Conclusion

Effects from the COVID-19 pandemic on the memory markets have been immediate and dramatic and are expected to continue impacting the memory markets into the foreseeable future. Although there has been some demand upside in the near term due to changing work, education, and leisure habits, the long-term economic impacts are likely to be severe, and hamper demand in the mid- to long-term. It is imperative that the memory suppliers respond proactively and with caution given the uncertainty in the markets to ensure the long-term health of the memory industry. Yole will continue to closely monitor the entire supply chain and adjust our outlook as needed.

About the authors

Walt Coon joins Yole Développement’s memory team as VP of NAND and Memory Research, part of the Semiconductor & Software division. Based in the US, Walt is leading the day-to-day production of both market updates and Market Monitors, with a focus on the NAND market and semiconductor industries. In addition, he is deeply involved in the business development of these activities.

Walt has significant experience within the memory & semiconductor industry. He spent 16 years at Micron Technology, managing the team responsible for competitor benchmarking, and industry supply, demand, and cost modeling. His team also supported both corporate strategy and Mergers & Acquisitions analysis. Previously, he spent time in Information Systems, developing engineering applications to support memory process and yield enhancement.

Mike Howard is a member of the memory team at Yole Développement (Yole) as VP of DRAM and Memory Research. Mike’s mission at Yole is to deliver a comprehensive understanding of the entire memory and semiconductor landscape (with special emphasis on DRAM) via market updates and Market Monitors. Mike is also deeply involved in the business development of all memory activities. Mike is based in the US.

Mike has a deep understanding of the DRAM and memory markets with a valuable combination of industry and market research experience. For the decade prior to joining Yole, Mike was the Senior Director of DRAM and Memory Research at IHS. Before IHS, Mike worked at Micron Technology where he had roles in corporate development, marketing, and engineering.