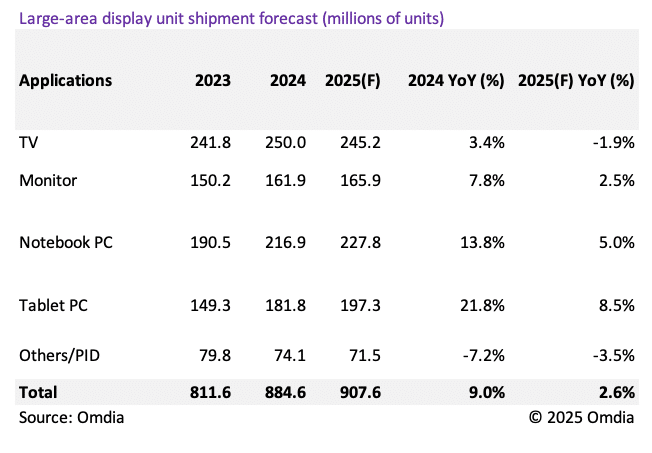

According to Omdia’s latest Large-Area Display Market Tracker, large-area (above 9-inch) display unit shipments are forecast to grow by 2.6% year-over-year (YoY) in 2025. However, this marks a slowdown compared to 2024, as global economic uncertainty and US tariff concerns weigh on the market.

TV and Others/PID application are expected to post negative growth, with the overall outlook reflecting industry caution amid potential recession risks. Notably, Sharp ceased LCD TV display production at its Gen 10 fab in 3Q24 and Chinese panel makers are taking a conservative approach to increasing LCD TV display shipments to help stabilize panel prices. Shipments in the Others/PID category remain highly sensitive to broader economic conditions.

“It is a forecast, that large-area LCD unit shipments will increase by 2.0% YoY and shipment area will grow by 3.9% YoY in 2025. This growth is significantly slower than in 2024. Panel makers are concerned about possible demand erosion in the second half of 2025 due to front-loaded panel purchasing in 1Q25 and the risk of a potential economic recession. As a result, they are becoming more conservative in their production plans and are focusing more on shipment area growth rather than unit growth. Consequently, LCD TV display unit shipments are forecast to decline by 2.2% YoY while shipment area is expected to increase by 4.6% YoY in 2025. Panel makers are also cautious about the monitor LCD segment, which is projected to grow by only 1.8% YoY due to poor financial results.” said Peter Su, Principal Analyst of Omdia.

“Large-area OLED shipments are projected to rise 20.4% YoY in units and 12.9% YoY in area in 2025 – a slower growth rate compared to 2024. Tablet PC OLED shipments are expected to decline by 1.8% YoY with Chinese makers reducing output by 9.2% YoY while Korean makers see a slight increase of 1.2% YoY. The OLED tablet segment has faced challenges in China due to high prices. However, Chinese makers are expected to increase their notebook PC OLED shipments by 5.4% YoY in 2025 while total notebook PC OLED shipments are forecast to surge by 47.0% YoY. OLED TV shipments are also expected to rise thanks to aggressive expansion plans from Korean TV brands. Meanwhile, OLED monitor and notebook PC OLEDs are projected to see double digit growth in 2025 fueled by strong strategies from Korean OLED makers,” added Su.

Total large-area display revenue is forecast to reach $72.7 billon in 2025 representing a 3.5% YoY growth. This marks a slowdown from the 14.8% YoY revenue growth in 2024 which reached $70.3 billion due to rising shipments and LCD TV display price hikes. While overall shipment growth will be slower in 2025, revenue is expected to grow at a faster rate than units driven by ongoing size migration particularly in TVs. Large-area display shipments area are projected to increase by 4.3% YoY in 2025 outpacing unit shipments in the same period.